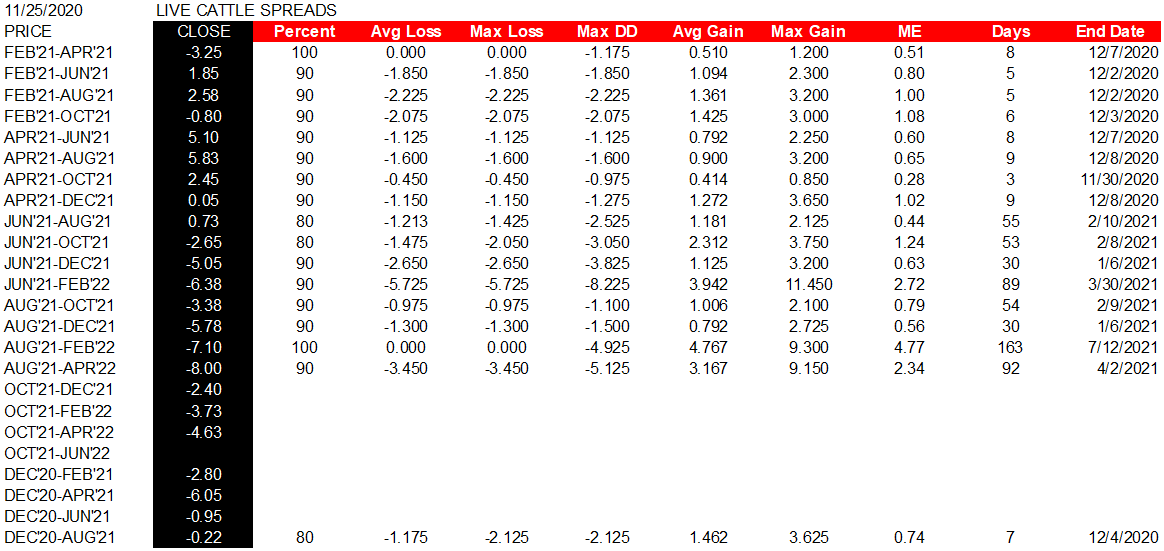

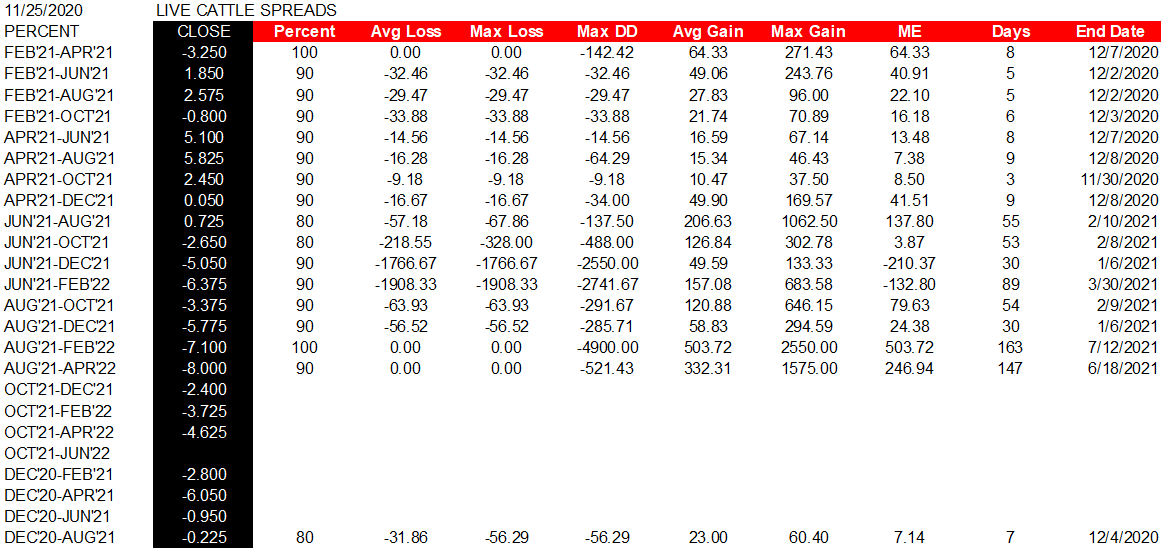

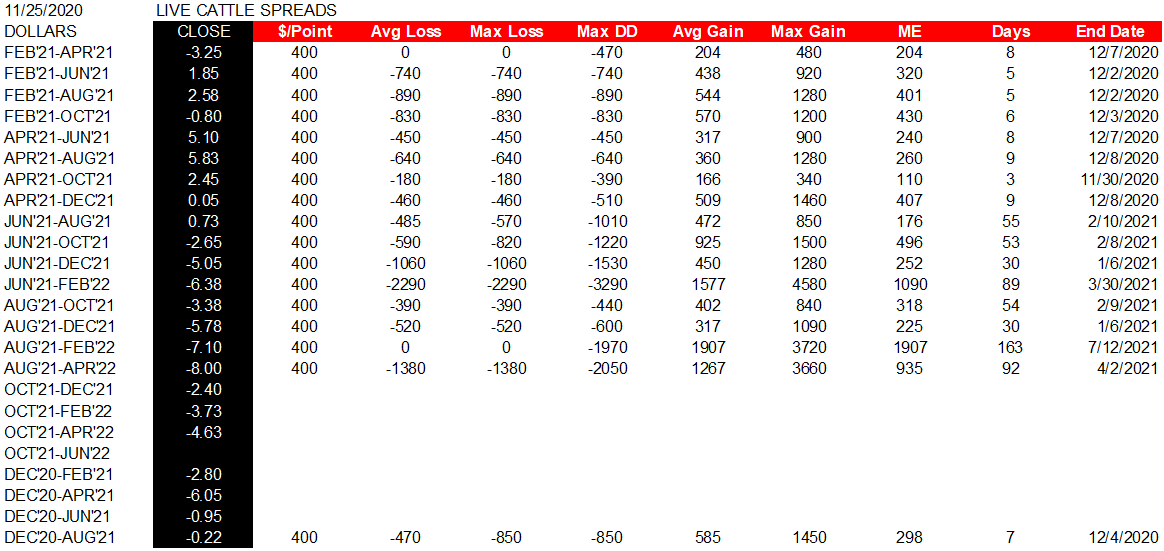

GLOSSARY

Entry Date’ is stated on the date stamp at the top left of the table. All strategy metrics are calculated using settlement prices.

The first column lists the individual strategies using their exchange listed symbols wherever possible. For clarification a list of these symbols and their long-form descriptions are available in the List of Markets link at the bottom of the Homepage.

The second column indicates the settlement price for that particular strategy using that day’s settlement price.

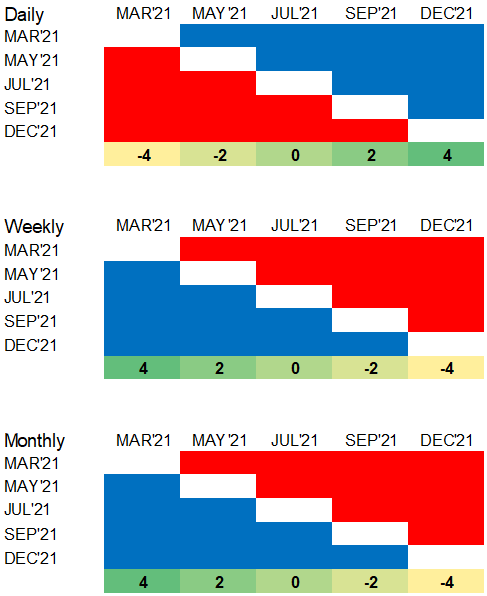

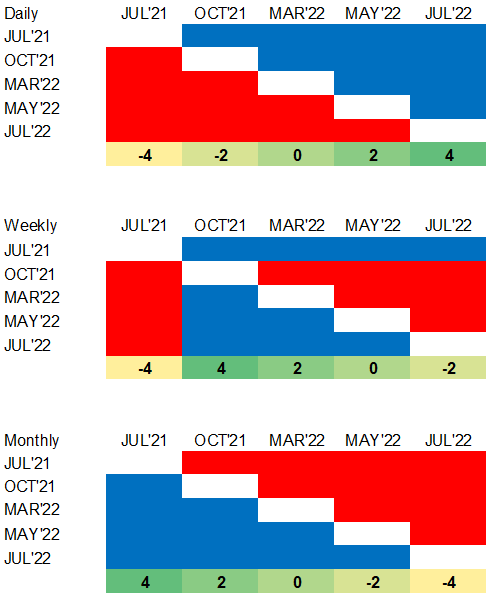

The red bar at the top with white text indicates that the strategy is a short strategy. Long strategies are depicted in blue.

The ‘Percent’ column details the win rate in percentage terms over the past 10 years for the specific strategy during its holding period (entry on November 26th 2020, exit on the ‘End Date’).

The ‘Average Loss’ column gives the historical Average Loss for the strategy over the past 10 years from the Entry date to the ‘End Date’.

The ‘Maximum Loss’ column details the historical maximum loss incurred for the strategy during the holding period over the past 10 years.

The ‘Maximum Drawdown’ column states the historical maximum loss from peak to low equity over the past 10 years during the holding period.

The ‘Average Gain’ column gives the historical Average Gain over the past 10 years for the strategy from the Entry Date to the ‘End Date’

The ‘Maximum Gain’ column details the historical maximum gain over the past 10 years for the strategy during the holding period.

‘ME’ is a conservative risk-adjusted return ratio calculated using Maximum Drawdown versus Average Loss. It is calculated as E(X)=E(X+)-E(X-), where Expected Value = Probability of Gain x (Average Gain) – Probability of Loss x (Maximum Drawdown).Strategies with Expected Values greater than 0 are preferred over those strategies with negative values.

‘Days’ is the total number of days (calendar days, not including weekends) in the strategy holding period.

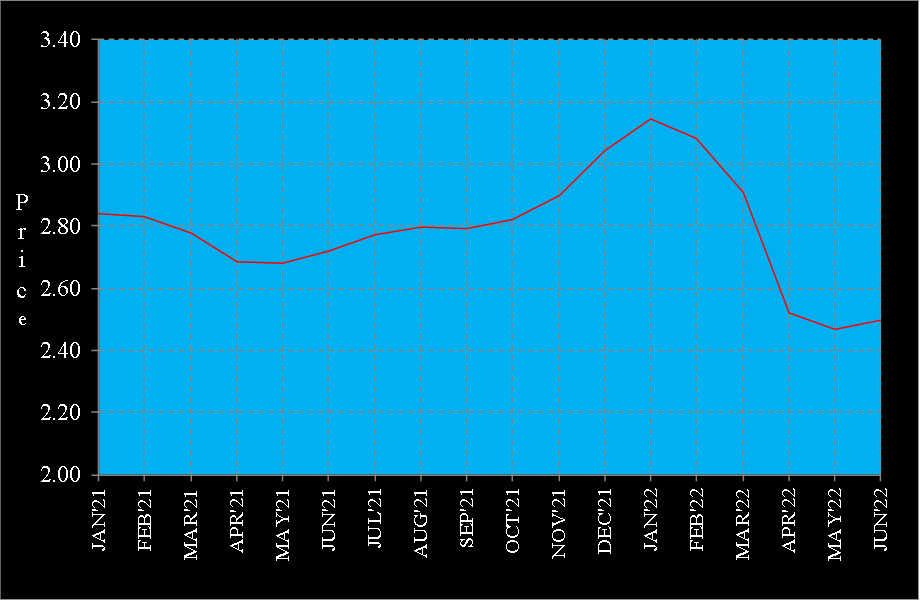

TERM STRUCTURE CHARTS

Commodity calendar spread strategies are provided with term structure charts that are updated daily and illustrate forward curve pricing showing the degree of prevailing contango and backwardation that exists. It is also useful in identifying opportunistic strategies driven by temporary aberrations in the curve shape due to temporary supply and demand shocks typically caused by weather and geo-political factors. The term structure illustrated below is the forward curve for Henry Hub Natural Gas futures extending to the June 2022 contract as of the close of trading on November 27th 2020.